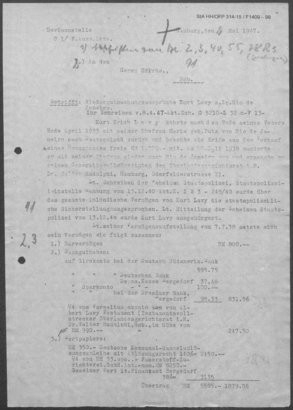

On May 2, 1947 Oberregierungsrat Fritz Klesper, head of the Hamburg State Office for Property Administration [Hamburger Landesamt für Vermögenskontrolle] (in charge of the administration of former National Socialist property and processing of “compensation” and restitution payments) which had only been established that year, sent a three-page letter to his superior, the President of Hamburg’s Main Finance Office. It concerned the “reparation claims” that Kurt Lavy had filed. A Jew from Hamburg-Bergedorf, Lavy and his wife Anna-Maria had fled to Rio de Janeiro in 1938. In his letter, Klesper referred to Gestapo files and Lavy’s statement of assets of July 8, 1938. To assess the value of Lavy’s former ownership share in the Bergedorf company Faserstoff-Zurichterei GmbH [a pulp processing plant], he used a market value reduced to 38 percent, which the Bergedorf tax office had suggested in 1938 for “Aryanization purposes.” Reichsstatthalter Karl Kaufmann, who had authorized the company’s “Aryanization” in 1938, had set the corresponding depreciation at 50 percent, however. Klesper was aware of this in 1947. He had been head of the surveillance and criminal departments at the Exchange Control Office [Devisenstelle] from 1937, which at that time was already reporting to the Chief Finance President and, together with the Gestapo and Customs Investigation Office, had plundered the Jews who had been forced to leave the country. After 1945, when he continued his career at the State Office for Property Administration [Landesamt für Vermögenskontrolle], of all places, he used the particularly extreme “Aryanization calculations” of the Bergedorf tax office in 1938, thus recommending a second expropriation of Lavy’s company property in 1947.

During the National Socialist regime, the German tax authorities participated in robbing the German Jews of their property. After 1945, they made every effort to block attempts at restitution and compensation in the Western occupation zones and in the Federal Republic of Germany. On a regional level (especially for Bremen and Bavaria, but also to some extent for Hamburg), this has been well researched and documented. The National Socialists pushed Jews out of the business sector. In Hamburg, the authorities reporting to the Chief Finance President, namely the Exchange Control Office, the Customs Investigation Office and the Gestapo, organized this legalized robbery. The significant role the local tax offices played in this process is much less known. Using the example of the tax office Hamburg-Bergedorf shows that these offices were not run by apolitically loyal officials. In their majority, the tax officials must be counted among the Nazi perpetrators. Beginning in 1933, the tax authorities systematically discriminated against Jewish citizens. The next step consisted in the orchestrated robbing of Jewish emigrants. The sums extorted in the process made a substantial contribution to German armament. The antisemitic measures of the higher tax authorities were eagerly supported by the local tax offices.

A general overview:

Kurt and Anna-Maria Lavy lived in the Bergedorf family villa (Schlebuschweg 5) from 1933 to 1938. Kurt Lavy was a successful engineer and businessman. As one of a four-member community of heirs, which held almost half of the capital of the Bergedorf company Faserstoff-Zurichterei GmbH [a pulp processing plant], he was co-owner and managing director of the company. The community of heirs also owned property in Bergedorf, including the Lavy Villa. Born a “non-Aryan” in 1895, as recorded in the “Questionnaire for Emigrants” dated July 7, 1938, Kurt Lavy fled to Brazil with his “Aryan” wife Maria Lavy, née Pütz (born 1897), at the end of July 1938. Bergedorf National Socialists had organized antisemitic riots outside their house and the factory. Anna-Maria Lavy subsequently suffered a miscarriage. The company no longer received any government contracts because its ownership was partly Jewish, and it was increasingly discriminated against in terms of foreign exchange law. Kurt Lavy was pushed out of the management, and the Jewish share of the business was prepared for “Aryanization” from spring 1938. In 1938, the Hamburg-Bergedorf tax office was directly or indirectly involved in almost all measures with which the Lavys were almost completely plundered before their escape: An “Emigration Tax payment” in the amount of approx. RM 2,000 foreign exchange audits at the company by the Exchange Control Office (June 23, 1938); an order to seize company assets issued by the Customs Investigation Office (July 13, 1938), whereby Kurt Lavy lost all control rights over the company; Dego tax on removed personal property (July 4, 1938) of RM 1,068; “Aryanization” of his company share and the villa. On November 12, 1938—almost four months after his flight—Kurt Lavy was also required to contribute RM 1,600 to the Jewish property tax [Judenvermögensabgabe], which was deducted from the blocked account. On December 13, 1940 all his domestic assets, including the blocked account, were “declared confiscated by the state police.” The National Socialist state had expropriated him for good. At the same time he and his wife were expatriated. The assets of expatriates automatically fell to the German Reich. With the “Decree of the Führer and Chancellor of the Reich on the Realization of the Confiscated Assets of Enemies of the Reich” [“Erlass des Führers und Reichskanzlers über die Verwertung des eingezogenen Vermögens von Reichsfeinden”] (May 29, 1941), the Reich Treasury Administration in Berlin rose to become the key authority. The couple arrived in Brazil completely impoverished. Both fell seriously ill after a short time. Kurt Lavy had to accept a job as a low-paid fitter in a chemical factory since he would not have been able to obtain a Brazilian entry visa otherwise. Shortly after arriving in Brazil, he suffered a chemical accident, inhaled chlorine gas and developed symptoms similar to those of poison gas victims of World War I. Anna-Maria Lavy suffered from severe depression due to the constant pressure of persecution in Germany and fell ill in the humid climate of Brazil. The Lavy couple managed only slowly to build up a modest new existence.

On 26 April 1938, within the framework of the four-year plan (whose goals were the financing of rearmament and self-sufficiency), Hermann Göring had issued an ordinance on the registration of Jewish property. This initiated the complete exclusion of German Jews from the economy and its final “Aryanization”. The tax offices were among the most important hinges for the implementation of this legalized robbery. Starting in May 1938, the Bergedorf tax office initially responded meticulously to inquiries from the Gestapo and the Exchange Control Office regarding domestic and foreign assets held by the Lavy family. It requested an updated declaration of assets from Kurt Lavy, which it received on July 8, 1938. Previously, it had already determined the value of his “Jewish” company share and, in preparation for its “Aryanization”, calculated drastically downwards—to 38 percent! Kurt Lavy was forced to enter this 38 percent, as determined by the tax office, both in the appendix to the “Questionnaire for Emigrants” and in his new declaration of assets. Instead of RM 8,250, it was now assumed to be RM 3,135. This was a particularly assiduous and radical proposal, as even the highest National Socialist in Hamburg, NS-Gauleiter and Reich Governor Karl Kaufmann, apparently found 38 percent to be exaggerated and on October 31, 1938 he determined the “Aryanization price” of the Jewish company shares at 50 percent. But whether the market value of Jewish company property was reduced to 38 or “only” to 50 percent was of no importance to the persecuted Jewish owner at the time. Lavy was deprived of 100 percent of his share in the company—along with almost all other assets—because everything that the “Aryanization profiteer” Paul Rode paid into Lavy’s “emigration escrow account” [Auswanderersperrkonto] was confiscated in 1940/1941 without replacement. The Jewish part of the company’s pulp processing plant was “Aryanized”, i.e. sold forcibly, at half of its actual value in the fall of 1938. And the Lavy Villa, which in 1939 had a market value of at least RM 31,000, was placed under forced administration at the beginning of 1939, which carried out the “Aryanization” for just under RM 24,000. The “Aryanizer” in both cases was Paul Rode.

It was these 38 percent and not even the 50 percent determined by Karl Kaufmann that Fritz Klesper used for his calculation of Kurt Lavy’s “restitution claims” in 1947. Klesper wrote on the first page of his letter: “Faserstoff-Zurichterei GmbH. Ant.-nom. RM 8,250,- Common value according to Bergedorf tax office 38 % = 3135.” Klesper himself had reported in a letter to the Reich Minister of Economics on 8 August 1938 that the ownership share of the Jewish community of heirs, which in itself amounted to RM 33,000, had been “Aryanized” for 16,500, i.e. in fact for 50 percent. Klesper knew what he was doing in 1947. Formally speaking, he did not make a mistake, since, as he himself stated, he only quoted from Kurt Lavy’s 1938 declaration of assets. It comes as no surprise that he did not make the “Aryanization” as such a “reparation matter,” because it was only indirectly mentioned in Lavy’s declaration of assets with the 38 percent, but in 1938 (!) it could not be addressed at all. Klesper was no stranger to Hamburg Jews who had fled Germany. From 1937 on, he had been head of the surveillance and criminal investigation department at the Exchange Control Office, which reported to the Chief Finance President in Hamburg and, together with the Gestapo and the Customs Investigation Office, had aggressively seized the property of fleeing Jews. After 1945, Klesper continued his career in the tax office, of all places, at the Hamburg State Office for Property Administration established in 1947, where he became responsible for “reparations” and restitution payments. If Lavy had expected that Klesper would examine his “restitution claim” objectively and neutrally, he was deceived like the other members of the community of heirs and like many of his Jewish fellow sufferers. Klesper’s calculations of Kurt Lavy’s claims for company and real estate shares totaled approximately RM 14,400. Klesper still calculated in Reichsmark, which was already largely worthless at that time. After the currency reform (June 20, 1948, devaluation of 10 RM to 1 DM), Kurt Lavy would only have been entitled to about 770 DM. The compensation payment to Kurt Lavy and to the community of heirs proposed by Klesper amounted to just 18 percent of what they were later awarded in DM as part of a compromise settlement. The compromise with the “Aryanizer” Paul Rode of August 7, 1951 was still unfavorable for the community of heirs. The villa was returned to them, but in the course of an out-of-court settlement they had to give up their share of the company for a small fee.

Fritz Klesper’s letter proves two things: In the “Aryanization” of the Lavy family’s company assets in 1938, the tax office in Hamburg-Bergedorf tried to go far beyond what leading Hamburg National Socialists considered the usual procedure. It also makes clear that the former head of the surveillance and criminal department of the Nazi Exchange Control Office, Senior Government Councillor Fritz Klesper, was able to continue his career in 1947 in the Hamburg Office for Property Administration and, in the case of Kurt Lavy, to make a second attempt at plundering. In his letter, he also recommended a consultation with Lavy’s authorized representative, Dr. Walter Rudolphi. Rudolphi would be able to provide more detailed information about the sale, i.e. the “Aryanization” of the Lavy villa and about the confiscation of Kurt Lavy’s remaining assets in Germany “by the German Reich,” he noted. Klesper knew very well that this respected lawyer and Higher Regional Court Counselor [Oberlandesgerichtsrat], whom the National Socialists had driven out of office in 1933 since he was Jewish, had been murdered in Auschwitz in 1944. To call upon him as a witness twice in his letter reveals his obvious contempt for humanity and his utter cynicism.

This text is licensed under a Creative Commons Attribution - Non commercial - No Derivatives 4.0 International License. As long as the work is unedited and you give appropriate credit according to the Recommended Citation, you may reuse and redistribute the material in any medium or format for non-commercial purposes.

Bernhard Nette, born in Hamburg in 1946, studied history and German literature at the University of Hamburg from 1968–1973, followed by research and teaching at Oxford University from 1974–1976. Between 1978–2011 he taught German and history at a comprehensive school and was on the state board of the local teachers’ union, GEW Hamburg from 1995–2010. He is the author of: Die Lehrergewerkschaft und ihr "Arisierungserbe." Die GEW, das Geld und die Moral, Hamburg 2010 (with Stefan Romey); "Vergesst ja Nette nicht!" Der Bremer Polizist und Judenreferent Bruno Nette, Hamburg 2017; Ausplünderung: Bergedorfer Juden und das Finanzamt. Beispiele von NS-Verfolgung und "Wiedergutmachung," Hamburg 2019.

Bernhard Nette, The Role of the Hamburg-Bergedorf Tax Office [Finanzamt Hamburg-Bergedorf] and the Hamburg Exchange Control Office [Hamburger Devisenstelle] in the Twofold Plundering of the Jewish Lavy Family in 1938 and 1947–1951 (translated by Insa Kummer), in: Key Documents of German-Jewish History, July 01, 2020. <https://dx.doi.org/10.23691/jgo:article-261.en.v1> [August 05, 2026].