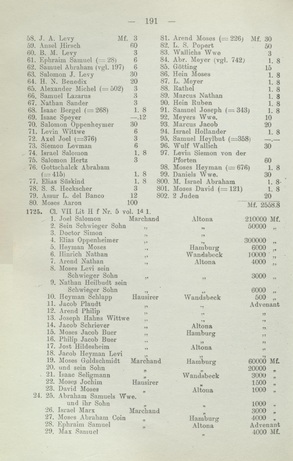

The present documentary source is a brief excerpt from tax lists of the early modern period, reproduced in Max Grunwald’s 1904 local history: “Hamburgs deutsche Juden bis zur Auflösung der Dreigemeinde 1811” [“Hamburg’s German Jews up to the Dissolution of the Triple Congregation 1811”]. The tax lists printed therein cover the years 1716, 1725, and 1734. The 1716 list records approximately 100 entries along with the amount of tax paid. For the year 1725 there are about 700 entries, detailing individual occupational activities, residential locations, and reported assets. For 1734 only the 124 Jews of Wandsbek are recorded; in addition, the total number of Jews in Hamburg and Altona is specified. Because of its relative comprehensiveness, the tax list of 1725 will be taken as an example. Consideration of the tax records of 1725 recommends itself because they were compiled after the exemption from regulations occasioned by the plague and war years but before the economic crisis of the late 1720s. Thus, they afford a representative view into a few aspects of Jewish life in Hamburg during the early modern era.

Tax lists were compiled by the elders of the Jewish congregation, before whom all Jews had to appear every three or four years in order to declare, under oath, their total assets. On this basis the elders decided the amount of tax owed. These varied because the Senate and city assembly’s determination of the annual amount of tax to be paid was periodically revised. The congregation’s internal bureaucratic procedure served the purposes of collecting, storing, controlling, and justifying the individual taxpayer’s contribution. The tax lists published by Grunwald have been digitized and are accessible online in the Frankfurt Freimann-Collection.

The tax documentary records afford important insights into the family relations, occupational structure, income distribution, and residential districts of the Jewish population in the early modern era.

The Jewish congregations in and around Hamburg joined together in 1671 as the triple congregation Dreigemeinde AHW, signifying the large Jewish communities of Hamburg, Altona, and Wandsbek. In the 18th century Jews tended to prefer living in Altona than in Hamburg or Wandsbek. According to the tax list of 1725, almost twice as many Jewish taxpayers lived in Altona than in Hamburg; a minority of Jewish co-religionists lived in Wandsbek. The 18th century is considered the heyday of Altona’s Jews because Danish Altona afforded them favorable conditions and because the Hamburg markets, where they plied their trades, were not far distant. The tax records substantiate the presence of extraordinarily wealthy Jews in Altona. For example, the fortunes of Joel Salomon, Elias Oppenheimer, and Elias Salomon, taken together, amounted to 710,000 Reichstaler; Saloman Berens’ fortune amounted to 1,600,000 Reichstaler. At the beginning of the 18th century, conditions for Jews in Hamburg were uncertain. It was only after passage of the New Regulation on Jews in 1710 that Jews were no longer restricted to certain districts but were officially permitted to live anywhere. To be sure, Jews had lived in Hamburg since the 17th century, but because of their uncertain legal status it was repeatedly possible to expel them to Altona. The passage of the New Regulations marked a turning point and the Hamburg Jewish congregation slowly began to flourish.

In the early 18th century, the common household must be comprehended as a living together under one roof of, not only biological children, but also stepchildren, illegitimate children, relatives, grandparents, and for the most part unmarried maids and male servants. The household was patriarchal in structure with a strict set of rules integrated into the normative world of the village or city society. It had important contributions to security and survival to perform. The tax lists specified the masters of the house or, after his death or in his absence, the mistress of the house who carried on the business. The remaining members of the household are not usually named in the tax lists but rather itemized solely according to their positions. For example list numbers 84-87 record “Isaac Jochim, wife, and children” or positions 109-110, “Michel Marx and his brother.” In general, the tax lists indicate few children, which can be attributed to the high child mortality rate in the early modern era. In many cases only half of the live births reached the age of 14, which is why few married couples had more than three or four children.

A peculiarity of the Jewish population was its widely ramified network of relatives. Often these relations reached far into the East, to Poland and Lithuania. The surnames of those mentioned in the tax lists disclose the familial places of origin. The excerpted tax lists document persons from the vicinity, such as Halberstadt, Hamm, and Wunstorf, but indicated more distant origins as well, such as Berlin, Amsterdam, Copenhagen, and Danzig. The proximity of Hamburg to Denmark and Prussia, the close economic relations to the Netherlands and its important ports of trade, brought Jews from many German and foreign territories to Hamburg; some of them settled there and in its environs. The Jewish congregation in early modern Hamburg comprised Jews from a wide variety of places of origin. The Jewish community not only possessed a high measure of mobility, and its members thus traveled, sometimes over great distances, but also utilized far-flung family relations, profiting from them in their business activities.

On the basis of mid-18th century tax lists, Grunwald indicates the occupational distribution of Hamburg’s Jews as follows: “278 merchants, 28 schoolmasters, 20 scholars, 3 ‘tutors’, 2 language teachers, 3 musicians, 4 physicians, 1 postman, 1 weapons dealer, 1 dyer of old hats, 1 gatekeeper, 1 ‘cane-maker Jew’ , 11 ‘who live on their own means’, but only one of whom operates as a pawnbroker.” Max Grunwald, Hamburgs Deutsche Juden bis zur Auflösung der Dreigemeinde 1811, Hamburg 1904, p. 60. By contrast, the earlier tax lists of 1725 list almost exclusively retailers and peddlers, of whom approximately 60 percent were numbered among the better-off merchants and 40 percent among the less well-off peddlers. Apparently, the occupations were not so precisely delineated in 1725, and because of the absolute dominance of merchants, other occupational groups were not listed or were noted on separate lists which have not been preserved. Moreover, Jews had long been excluded from the guilds and could not become craftsmen. Similarly, next to no Jews worked in agriculture, which occupied a great part of the population. The extended family networks of Jews were of great advantage in commerce. Their relatives not only provided them with important information and provided distant contact points, but frequently they also actively helped conduct business by making purchases or even undertaking commercial trips themselves. In this respect, Jewish businessmen often had an advantage over their Christian competitors. The wealth and esteem of the great merchants also benefited the triple congregation Dreigemeinde AHW, for example, with the negotiations for tax reductions during the plague years, crucial to the Jewish congregation. In contrast to Christians, Jews were reliant upon letters of protection which assured them the right of establishment in a specific place when paying a special fee. Oftentimes, these were not continued, nor were they extended to the children of so-called protected Jews, owing to the fact of their high degree of mobility and that family members often lived in other cities, territories, or countries.

Following the Thirty Years’ War, the demography of the Jewish congregations altered markedly. Triggered by the waves of Jews fleeing from the East, for example, in the wake of the Cossack revolts Uprisings in the years 1648 and 1649 carried out by the Russian and Cossack population against the Polish nobility, also directed against Jews and Jesuits., the Jewish population of Hamburg rose. This in turn led to a sharp growth of the Jewish underclass, whose proportion of the total Jewish population in the 18th century is estimated at 90 percent. This development required the raising of additional financial means from within the Jewish congregations because they alone were responsible for the care of their poor. The Jewish congregation’s increased need for money is reflected in the tax lists by the high tax expenditures of individual congregation members. Wealthy Jews were obliged to set aside 0.5 to 1 percent of their total wealth with which to pay for those unable to pay their own taxes. In the tax levy of 1716 Elias Oppenheimer once again stands out because of the relatively high tax of 200 Reichstaler. Nine years later, according to the tax documents of 1725, his fortune amounted to 300,000 Reichstaler. Furthermore, updated information from a later point in the same year fixed his total capital at 400,000 Reichstaler and his tax obligation at approximately 1 per cent, that is, 4,061 Reichstaler. From this example it can be seen how high the tax burden of congregation members was, as well as how the financial circumstances of individual Jews can be tracked by means of the tax lists.

Grunwald ascribed such high significance to Hamburg taxation that he started off his description of the conditions of Hamburg’s Jews in the 18th century with a chapter on the taxing power of the Jewish congregation. In view of the difficult situation with regard to original source materials, even today the tax documentation still affords an outstanding – and in many cases the only – possibility for learning about specific aspects of Jewish life in early modern Hamburg.

This text is licensed under a Creative Commons Attribution - Non commercial - No Derivatives 4.0 International License. As long as the work is unedited and you give appropriate credit according to the Recommended Citation, you may reuse and redistribute the material in any medium or format for non-commercial purposes.

Nadja Hauptvogl, born in 1990, studied theology, religious studies and English studies. In 2015 she received a master degree in Jewish history at the Leo Baeck Institute at Queen Mary University of London.

Nadja Hauptvogl, Tax Lists of the Early Modern Period: Insights Regarding Jewish Life in Pre-modern Hamburg (translated by Richard S. Levy), in: Key Documents of German-Jewish History, September 27, 2017. <https://dx.doi.org/10.23691/jgo:article-170.en.v1> [August 03, 2026].